Small Business Tax Deductions: The Complete 2026 List

Most small business owners overpay their taxes because nobody gave them the full deduction list with actual rules. This guide covers every major deduction available in 2026: home office, mileage, retirement contributions, health insurance, SE tax deduction, and equipment. All with exact numbers and IRS sources.

This article is for educational and informational purposes only and does not constitute financial, tax, legal, or accounting advice. Groundwork is not a licensed financial advisor, accountant, or attorney. Before making decisions, consult a qualified professional.

Small business tax deductions reduce your taxable income before any rate is applied. The ones most owners miss: the home office deduction ($5 per square foot up to 300 sq ft on the simplified method), business mileage ($0.725 per mile in 2026), deducting half of your self-employment tax from gross income, health insurance premiums if you pay for your own coverage, and Solo 401k contributions (up to $24,500 in employee contributions for 2026). None of this requires an accountant to understand. You need this list and a habit of tracking expenses every week.

- Why most small business owners pay more tax than they owe

- The complete 2026 small business tax deduction list

- The 5 deductions most owners never claim

- Home office deduction: what actually qualifies

- Vehicle and mileage: the exact rules

- Using retirement contributions to reduce your tax bill

- What records to keep and for how long

- Frequently asked questions

You paid your taxes, felt the sting, then heard from someone at a networking event that they wrote off their car, their phone, and half their rent. You nodded and said you do that too. You did not do that.

Most small business owners have a vague sense that deductions exist and a specific anxiety that they are not claiming enough of them. They are usually right. Not because deductions are hidden or complicated to access, but because nobody has ever put the full list in front of them with the actual rules for each one in plain language. This guide does that.

Why most small business owners pay more tax than they owe

When you work for an employer, your taxes are calculated for you. Withholding is automatic, your W-2 arrives in January, and you file what the numbers say. Running your own business does not work that way. Self-employment tax is 15.3% of your net earnings, covering both the employer and employee share of Social Security and Medicare. On top of that sits your ordinary income tax. If your business cleared $80,000 in profit this year, you could easily owe $20,000 or more in combined taxes before a single deduction is applied.

Every legitimate deduction you take reduces the number that all of those rates are applied to. A $5,000 deduction at a combined 30% effective rate saves you $1,500 in actual cash. Miss five such deductions and you have overpaid by $7,500, not because the tax code is working against you but because you did not know what to claim. That is the whole problem and it has a straightforward fix.

The number that trips most people up is the combined rate. I went through IRS Topic 554 to get the exact breakdown rather than quoting it from memory:

The deduction most owners do not know is automatic. The IRS lets you deduct 50% of your self-employment tax directly from your gross income when calculating your adjusted gross income. This happens on Schedule SE before your taxable income is even calculated. If you paid $8,000 in SE tax, $4,000 comes straight off the top. Most small business owners who do their own taxes via software get this automatically. Most who do not know about it are surprised when an accountant points it out.

The complete 2026 small business tax deduction list

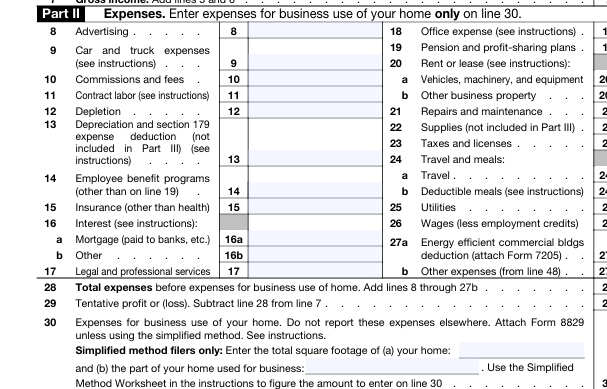

These are the deductions available to most small business owners in the United States for the 2026 tax year. They are reported on Schedule C of your Form 1040 if you operate as a sole proprietor or single-member LLC. Read through the full list before you decide what applies to you. Most business owners are surprised by at least three items they had not been tracking.

Most people have never actually looked at Schedule C before they file it. Worth seeing at least once. This is the real form, pulled straight from IRS.gov:

Advertising and promotion:100% deductible

Ads, sponsored posts, business cards, website costs, any spend to promote your business to potential customers.

Business meals:50% deductible

Meals with clients, partners, or employees where business is discussed. Keep the receipt and note who you were with and the business purpose. Company-wide social events are 100% deductible.

Business insurance:100% deductible

General liability, professional liability (E&O), commercial property insurance, and business interruption coverage. Personal life insurance is not deductible here.

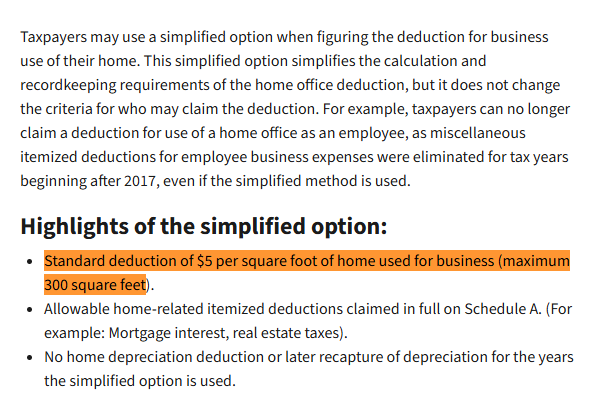

Home office:simplified method: $5 per sq ft up to 300 sq ft

The space must be used regularly and exclusively for business. A 200 sq ft dedicated office gives you a $1,000 deduction with zero calculation required. Full breakdown in the section below.

Vehicle and mileage:$0.725 per business mile in 2026

Client visits, supply runs, business errands. 5,000 business miles works out to $3,625 in deductions. Commuting to a fixed office does not count. Full rules in the vehicle section below.

Contract labor:100% deductible, 1099-NEC required at $600+

Payments to freelancers and independent contractors are fully deductible. If you pay any single contractor $600 or more in a calendar year, you must file a Form 1099-NEC or lose the deduction.

Professional services:100% deductible

Accounting fees, legal fees, bookkeeping, consulting. The cost of the accountant who prepares your business taxes is itself deductible as a business expense.

Education and professional development:100% deductible

Courses, books, conferences, and subscriptions that maintain or improve skills required in your current business. Training for a new career does not qualify. Training that makes you better at the work you already do does.

Software and subscriptions:100% deductible

Any software you use primarily for business: project management tools, design tools, accounting software, CRM, communication platforms, cloud storage. If you use a tool for both personal and business, deduct only the business-use percentage.

Phone and internet:business-use percentage deductible

If you use your phone 60% for business, deduct 60% of your monthly bill. If you have a dedicated business line, it is 100% deductible. Same logic applies to your home internet if you work from home.

Bank fees and merchant processing fees:100% deductible

Monthly business account fees, wire transfer fees, Stripe or PayPal processing fees, credit card annual fees on a business card. Small line items that add up over twelve months.

Business travel:100% deductible (meals at 50%)

Flights, hotels, and ground transportation for trips taken primarily for business. The IRS requires you to travel away from your tax home overnight for the trip to qualify. Meals during business travel are 50% deductible.

Equipment and assets:Section 179 or bonus depreciation

Computers, cameras, desks, printers, machinery. Under Section 179, you can deduct the full cost of qualifying equipment in the year you buy it rather than depreciating it over several years. Items under $2,500 can be expensed immediately under the de minimis safe harbor rule. Check IRS Publication 946 for the current year Section 179 limit.

Rent for business space:100% deductible

Office rent, coworking memberships, storage unit rental for business inventory. If you rent a dedicated space used only for business, the full amount is deductible without any of the home office rules applying.

Health insurance premiums:100% deductible if self-employed

If you pay for your own health, dental, and vision insurance and are not eligible for coverage through a spouse's employer plan, the full premium is deductible. This deduction comes off your gross income, not just Schedule C, making it particularly valuable.

Retirement contributions:deductible up to plan limits

Contributions to a Solo 401k, SEP-IRA, or SIMPLE IRA reduce your taxable income dollar for dollar. This is one of the most powerful tax levers available to a self-employed person. Full breakdown in the retirement section below.

The 5 deductions most small business owners never claim

You probably knew about advertising costs and software subscriptions. Here are the five that consistently go unclaimed, not because they are obscure but because nobody highlights them clearly enough.

The self-employment tax deduction

Half of your SE tax is deductible from gross income. If you paid $9,000 in SE tax this year, $4,500 comes off your adjusted gross income automatically. Tax software handles this, but if you do not know it exists you cannot verify it happened.

Health insurance premiums

Self-employed individuals who pay for their own health insurance can deduct 100% of premiums for themselves, a spouse, and dependents. At $500 per month, that is a $6,000 deduction most people leave on the table. The only condition: you cannot be eligible for coverage through an employer (including a spouse's employer plan).

Retirement contributions

Every dollar you put into a Solo 401k or SEP-IRA is a dollar that does not get taxed this year. At $24,500 in employee contributions plus a 25% employer contribution on top, this is the single largest legal tax reduction available to a self-employed person. Most small business owners either do not have one or do not contribute enough to notice the impact.

Home office

Most home-based business owners avoid this deduction because they have heard it triggers audits. It does not, and the myth has cost people a meaningful amount of money over the years. A 200 sq ft dedicated office space is worth a $1,000 deduction. A 300 sq ft space gets you the maximum $1,500 on the simplified method. With zero receipts required.

Phone and internet (partial)

If you use your phone 70% for business, 70% of your monthly bill is deductible. Same for your home internet. Nobody tracks this because it feels small, but $150 per month in phone and internet at 70% business use is $1,260 per year in deductions most people ignore entirely.

Home office deduction: what actually qualifies

The home office deduction has a reputation it does not deserve. The idea that claiming it raises your audit risk is a myth that has been circulating since the 1990s and has no basis in current IRS audit patterns. What it does have is a specific rule you must follow, and one word in that rule that disqualifies most people who try to claim it incorrectly.

That word is exclusive. The IRS requires that the space be used regularly and exclusively for business. A bedroom with a desk where you also sleep does not qualify. A dedicated room that you use only for work, even if it is a converted closet, does qualify. The exclusive use requirement is the entire test. If your office space passes it, you have a legitimate deduction.

I wanted to make sure the $5 per square foot rate had not quietly changed before writing this section. It has not. Here is the IRS page as it currently stands:

Simplified Method

How it works

Multiply your office square footage by $5. Maximum 300 sq ft. The most you can deduct is $1,500 per year. No receipts, no tracking actual expenses.

Best for

Renters and anyone who wants simplicity. Also avoids the depreciation recapture issue when you eventually sell your home.

Regular Method

How it works

Calculate the percentage of your home used for business (office sq ft divided by total home sq ft), then apply that percentage to your actual home expenses: rent or mortgage interest, utilities, repairs, insurance.

Best for

Homeowners in high-cost areas where actual expenses produce a larger deduction than $1,500. Requires Form 8829 and more documentation.

The business structure guide covers how forming an LLC affects your tax obligations, including whether you can still claim the home office deduction as an LLC owner. See the complete LLC vs sole proprietorship comparison for the relevant section.

Vehicle and mileage: the exact rules

If you drive for business, you are leaving money behind every time you do not log the trip. At $0.725 per mile in 2026, a single weekly client visit 25 miles away adds up to $1,885 in deductions over a year. Most small business owners who drive for work claim far less than they are entitled to because they do not track.

The 2026 rate is a bump up from last year and it is worth knowing exactly where that number comes from. IRS Notice 2026-10, published December 29, 2025, is the official source. This is what it says:

Standard mileage vs. actual expenses

Standard mileage rate

Track the miles driven for business, multiply by $0.725. Simple, no receipts for gas or maintenance required. Works best for fuel-efficient vehicles with moderate business use.

Actual expense method

Track every vehicle expense (gas, insurance, repairs, registration, depreciation), then multiply by the percentage of miles driven for business. More work, potentially larger deduction for high-mileage or expensive-to-operate vehicles.

What counts as a business mile: driving to a client meeting, picking up supplies, traveling between job sites, driving to a coworking space that is not your regular place of work. What does not count: driving from home to your regular office location. That is commuting and it is never deductible, regardless of how far it is.

The minimum you need to log for each trip: the date, the destination, the business purpose, and the miles driven. A mileage tracking app like MileIQ or Everlance does this automatically from your phone's GPS. The IRS requires contemporaneous records, meaning you cannot reconstruct a year of driving from memory in April.

Using retirement contributions to reduce your tax bill

A retirement account contribution is one of the few financial moves that is simultaneously good for your future and reduces your taxes today. Every dollar you contribute to a qualifying plan is a dollar that does not appear in your taxable income this year. At a 22% federal income tax rate plus 15.3% SE tax, each dollar shielded can save you close to $0.37 in combined taxes.

Solo 401k

In 2026, the employee contribution limit is $24,500. On top of that, you can contribute up to 25% of your net self-employment income as an employer contribution. This is the highest-capacity retirement plan available to self-employed individuals and the most powerful tax reduction tool on this list.

SEP-IRA

Simpler to open and maintain than a Solo 401k. You contribute up to 25% of your net self-employment income. No employee contribution component, so the total is lower than a Solo 401k for most people. The right choice if you want simplicity over maximum contribution capacity.

SIMPLE IRA

Designed for businesses with employees. Both you and your employees can contribute, and you are required to match up to 3% of employee compensation. Worth considering once you have staff, as the employer match is also fully deductible. Check the IRS COLA limits page for the current year employee contribution cap.

The math on maximizing a Solo 401k. If your business nets $100,000 and you contribute $24,500 as an employee plus a 25% employer contribution on your adjusted net earnings, your total annual contribution can approach $48,000. At a combined federal income and SE tax effective rate of around 35%, that is over $16,000 in taxes you do not pay this year. The money does not disappear, it grows in the account. You pay tax when you withdraw it in retirement, at whatever rate applies then, which for most people is lower than their working rate.

What records to keep and for how long

The IRS can audit your return for up to three years from the date you filed. If it suspects you underreported income by 25% or more, that window extends to six years. If it suspects fraud, there is no limit. Keeping records for seven years covers every realistic scenario.

Good accounting software solves most of this automatically. Every transaction is captured, categorized, and stored with a timestamp. For the items software cannot capture on its own, here is what you need.

Receipts for all business expenses

Photograph them immediately with your accounting app. Paper receipts fade and disappear. The IRS accepts digital copies. For meals, note the attendees and business purpose on the receipt or in the app at the time.

Mileage log

Date, starting location, destination, business purpose, and miles for every business trip. An app does this automatically. A handwritten log in the glove compartment works too. Neither works if you try to reconstruct it from memory at year end.

Bank and credit card statements

Download and store monthly statements as PDFs. Your bank keeps records but access is not guaranteed after a few years, and having your own copies speeds up any audit response dramatically.

Invoices and payment records

Every invoice you sent, every payment received, and every 1099 you issued or received. These are your income documentation. If your reported income ever needs verification, this is what you show. The right invoicing software generates these records automatically, manual spreadsheets are where audits go wrong.

Home office documentation

A floor plan or rough sketch showing the office space and square footage. Photographs of the dedicated work area help. For the regular method, keep all home expense receipts: utilities, rent or mortgage statements, insurance, and repair invoices.

Prior year tax returns

Keep every return you file plus all supporting documents for at least seven years. If you file electronically, download the PDF of your complete return immediately after filing and store it somewhere that is not just your tax software account.

The right accounting software captures the majority of this automatically by connecting to your bank and categorizing transactions in real time. The guide to the best accounting software for small business owners breaks down which tools handle deduction tracking best and which are worth the monthly cost. For the full picture of what your numbers should look like month to month, read the complete small business finance guide.

Frequently asked questions